Audit of Jordan's Principle

May 2025

Internal Audit Report

Prepared by: Audit and Assurance Services Branch

PDF Version (2.08 MB, 53 pages)

Table of contents

- Acronyms

- Executive Summary

- 1. Context

- 2. About the audit

- 3. Key findings and recommendations

- 4. Conclusion

- 5. Management action plan

- Annex A: Canadian Human Rights Tribunal (CHRT) Timeline and Key Orders

- Annex B: Audit Criteria

- Annex C: Departmental Expenditure Risk Levels

- Annex D: Examples of Approved Requests

Acronyms

- ADM

- Assistant Deputy Minister

- B2B

- Back to Basics

- CHRT

- Canadian Human Rights Tribunal

- DCI

- Data Collection Instrument

- FAA

- Financial Administration Act

- FNIHB

- First Nations and Inuit Health Branch

- FTE

- Full-Time Equivalent

- FY

- Fiscal Year

- G&C

- Grants and Contributions

- GCIMS

- Grants and Contributions Information Management System

- HQ

- Headquarters

- ISC

- Indigenous Services Canada

- JPCMS

- Jordan's Principle Case Management System

- MCF

- Management Control Framework

- O&M

- Operations and Maintenance

- SOP

- Standard Operation Procedures

Executive Summary

Canada has a legal obligation to ensure that First Nations children receive equitable access to health, social, and education services. Jordan's Principle, named in memory of Jordan River Anderson, a child from Norway House Cree Nation who died in 2005 at the age of five while federal and provincial governments disputed financial responsibility for his care, is intended to address service gaps and inequities.

Jordan's Principle is a demand-driven initiative that considers the unique circumstances of each First Nations child. Because it is not a formal program, it does not have fixed terms and conditions or a permanent source of funding. Instead, funding is allocated based on forecasted need and administered through a Special Purpose Allotment to maintain expenditure control. Decisions related to requests for products, services, and supports are guided by legally binding orders issued by the Canadian Human Rights Tribunal.

The Audit of Jordan's Principle was included in Indigenous Services Canada's Risk-Based Audit Plan for 2023–24 to 2024–25. It was presented to the Departmental Audit Committee on May 25, 2023, and subsequently approved by the Deputy Minister.

The objective of the audit was to provide assurance on the adequacy of the Management Control Framework supporting the ongoing implementation of Jordan's Principle, including the processes in place to minimize overlap in funding.

The audit found that the current implementation of Jordan's Principle, based on the Back-to-Basics approach, is unsustainable due to increasing demand, unclear eligibility criteria for expenditures, and an evolving scope of approved products and services, all within the constraints of departmental human and financial resources. To address these challenges, the audit also identified several opportunities to improve the Management Control Framework. These improvements could support long-term sustainability, reduce processing errors, and limit unnecessary requests by streamlining access to supports. As a result, the audit identified the following recommendations:

- The Assistant Deputy Minister (ADM) of Jordan's Principle should establish a risk-based management control framework with clearly defined roles, responsibilities, and guidance for those involved in delivering and overseeing the implementation of Jordan's Principle across the Department.

- The ADM of Jordan's Principle should explore, and as deemed appropriate, implement solutions to increase processing efficiencies, which may include technological enhancements.

- The ADM of Jordan's Principle should implement a process supported by clearly defined policy to ensure that Jordan's Principle funding for products and services that overlap with other Indigenous Services Canada (ISC) programs and other levels of government (province and territories) is minimized.

- The ADM of Jordan's Principle should revisit the overall placement of how Jordan's Principle fits within the suite of Departmental programs and services, and should develop a framework to guide consistent and appropriate implementation of Jordan's Principle.

Statement of conformance

The audit conforms with the Institute of Internal Auditors' Global Internal Audit Standards and the Government of Canada's Policy on Internal Audit, as supported by the results of the Quality Assurance and Improvement Program.

Management's Response

Management is in agreement with the findings, has accepted the recommendations included in the report and has developed a management action plan to address them. The management action plan has been integrated into this report.

1. Context

1.1 Background

Jordan's Principle is a human rights principle that was established to ensure that children do not experience gaps or delays in accessing government services and that they are not denied government services because they identify as First Nations.

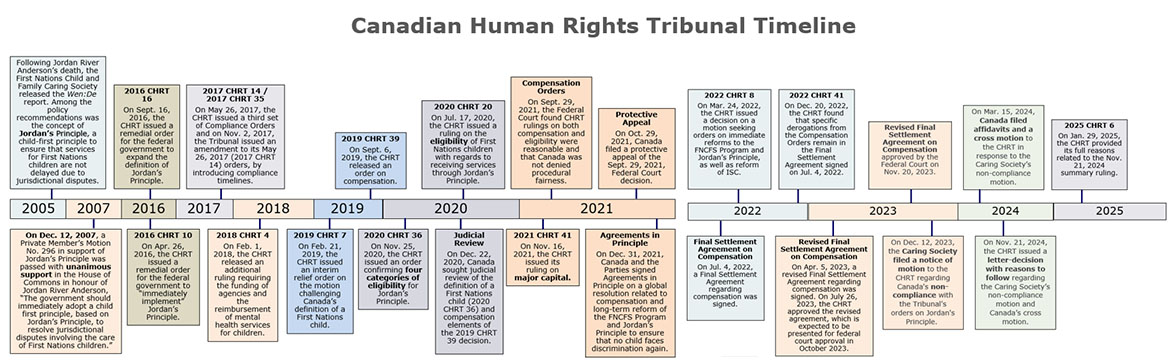

It is named in memory of Jordan River Anderson, a First Nations child from Norway House Cree Nation in Manitoba, who died in 2005 at the age of 5 in a hospital while the provincial and federal governments debated financial responsibility for his care in a medical foster home. Canada is obliged to implement Jordan's Principle in accordance with the Canadian Human Rights Tribunal (CHRT) orders.

In December 2007, the House of Common passed a unanimous motion: The government should immediately adopt a child-first principle, based on Jordan's Principle, to resolve jurisdictional disputes involving the care of First Nations children. While the motion was not legally binding, it represented a political commitment to uphold the principle that First Nations children should receive services first, and Governments should resolve funding disputes later. Between 2007 and 2014, Canada interpreted the principle narrowly, applying it only to cases of jurisdictional disputes rather than ensuring equitable access to services. This meant many First Nations children continued to face delays or denials of health, education, and social services. Successive reports by the Auditor General in 2011 and 2013 found persistent inequalities in funding for First Nations child welfare services and criticized the department for failing to address service gaps. In 2007, Cindy Blackstock and the First Nations Child & Family Caring Society (FNCFCS), along with the Assembly of First Nations (AFN), filed a human rights complaint against the Government of Canada. The complaint alleged that Canada discriminated against First Nations children by underfunding child welfare services and failing to properly implement Jordan's Principle. On January 26, 2016, the Canadian Human Rights Tribunal (CHRT) ruled that Canada was racially discriminating against First Nations children by underfunding child welfare services and failing to properly implement Jordan's Principle. The ruling ordered the federal government to fully implement Jordan's Principle to ensure First Nations children receive services based on substantive equality; stop interpreting Jordan's Principle too narrowly, and reform First Nations child welfare funding to eliminate discrimination. As part of its ruling, the CHRT determined that ongoing oversight was necessary to ensure Canada's full and proper implementation of Jordan's Principle. Accordingly, the Tribunal retained jurisdiction and oversight authority to monitor compliance and issue further orders as needed.

Jordan's Principle is a demand-driven initiative that considers the unique circumstances of each First Nations child to address inequalities and gaps in government services. Jordan's Principle does not have specific terms and conditions or a permanent source of funds. The approach to implementation stems from the Prime Minister's letter to the Minister in 2017 and policy authorities that were subsequently obtained in response to CHRT orders.

The policy authority derived from the Prime Minister's letter of 2017 expanded on previous policy authorities obtained through Cabinet decisions taken in July 2016. The impetus for this enhanced policy authority was the May 2017 CHRT order, which expanded the eligibility of Jordan's Principle to include all First Nations children both on and off reserve. Further, in 2017, the Minister obtained authority to:

- broaden eligibility from First Nations children living on reserve with a disability to all status First Nations children residing in Canada;

- expand the basket of services from health and social services and supports to include all publicly-funded health, social, and educational services or supports in Canada;

- eliminate the requirement for a formal jurisdictional dispute to provide culturally relevant funding and support that is in the best interest of the child under Jordan's Principle;

- supplement the current benchmark of normative standard of care with a process to assess all request in light of the objective of achieving substantive equality for First Nations children, and to help ensure effective, fair, consistent and reasonable decision-making; and

- establish process and criteria to expedite review of urgent requests with the objective, where possible, of initiating services within 12 to 48 hours. For non-urgent cases, provide at minimum an initial assessment and determination of cases within 12 to 48 hours.

Funding is allocated based on forecasted need and is administered through a Special Purpose Allotment to ensure expenditure control. Decisions made in response to requests for products, services and supports through Jordan's Principle are driven by the legally binding orders from the CHRT. Specifically, the CHRT ordered that services must be provided based on substantive equality—meaning that First Nations children should have access to services that account for their unique circumstances and historical disadvantages. This may necessitate funding for services go beyond that which applies to the normative standard (defined as the average or customary level of federal or provincial/territorial programs and services available). In the context of Jordan's Principle, substantive equality includes providing adequate supports to First Nations families to enable First Nations children to access substantively the same level of government services as other children, taking into account their distinct needs.

Since Jordan's Principle is a court-ordered initiative to ensure that First Nations children receive necessary services without delay, its implementation differs from Indigenous Services Canada (ISC) programs and their predefined budget allocations and terms and conditions. Rather, Jordan's Principle provides case-by-case responses to immediate needs.

1.2 Summary of CHRT order requirements

Since the 2016 CHRT ruling that determined that the Government of Canada's approach to services for First Nations children was discriminatory, ISC has pursued a renewed approach to Jordan's Principle. While the initial order clarified set out the core elements of Jordan's Principle, subsequent orders (refer to Annex A for more details) resulted in specific operational requirements that have dictated the implementation of Jordan's Principle rather than focusing on outcomes for First Nations children. The increased focus on operational elements has created an unsustainable implementation model that is reactive and limit the department's ability to policy guidelines and management controls. Key aspects of Jordan's Principle set out by the CHRT are listed below:

- Substantive equality, culturally appropriate services and best interests of the child should be evaluated.

- Jordan's Principle applies to all First Nations children, on or off reserve.

- Jordan's Principle addresses the needs of First Nations children by ensuring there are no gaps in government services for First Nations children.

- Government organization of first contact will pay for the service without engaging in administrative procedures.

- Case conferencing may still occur with professionals to better define the need.

- Reimbursement will be negotiated afterwards with other governments/departments.

To help ensure timely approval of requests, the CHRT has prescribed the following timelines in which ISC is required to approve or deny a request

| Type of request | CHRT timelines from point that all necessary information has been received. |

|---|---|

| Individual (urgent) | Within 12 hours |

| Individual (non-urgent) | Within 12 to 48 hours |

| Group (urgent) | Within 12 to 48 hours |

| Group (non-urgent) | Within 48 hours to 7 days |

1.3 Overview of how ISC implemented Jordan's Principle during the audit period

In January 2022, Canada announced Agreements-in-Principle (AIP) had been reached on a global resolution related to compensation for those harmed by discriminatory underfunding of First Nations child and family services and to achieve long-term reform of the First Nations Child and Family Services program and long-term approach of Jordan's Principle to ensure that no child faces discrimination again. The Agreements-in-Principle included:

- $20 billion in compensation for First Nations children on-reserve and in the Yukon, who were removed from their homes between April 1, 1991, and March 31, 2022, and for their parents and caregivers. This also includes compensation for those impacted by the government's narrow definition of Jordan's Principle between December 12, 2007, and November 2, 2017, as well as for children who did not receive or were delayed receiving an essential public service or product between April 1, 1991 and December 11, 2007.

- Approximately $20 billion, over five years, for long-term reform of the First Nations Child and Family Services program to ensure that the discrimination found by the CHRT never repeats itself. This includes funding to support young First Nations adults aging out of the child welfare system and prevention services to build on the multi-generational cultural strengths to help children and families in staying together that will be implemented as early as April 2022. There was also new funding for on-reserve housing to support these prevention initiatives.

The AIP included the Work plan to improve outcomes under Jordan's Principle which included streamlining operational procedures and the creation of Back to Basics. ISC implemented the agreed-upon Back to Basics (B2B) policy in early 2022with the vision to continue negotiations to reach a FSA on the long term approach of Jordan's Principle.

The objective of B2B was to ensure that the initiative was non-discriminatory; centered on the needs and best interests of the child; took into consideration the distinct circumstances of the child's community, and was simple to access, timely, and imposed minimal administrative burden on families. The B2B approach replaced a suite of standard operating procedures, which were perceived by some of the CHRT parties as being overly complex and misaligned with the intent of Jordan's Principle and the principle of Indigenous self-determination. The B2B policy guided implementation of Jordan's Principle for the audit period.

In addition to the roll out of the B2B approach, ISC Headquarters (HQ) was also responsible for determining escalated requests where a dedicated decision maker (DDM) either approved or denied an escalated request based on delegated decision-making authority from the First Nations and Inuit Health Branch (FNIHB) Senior Assistant Deputy Minister (ADM).

To promote awareness and help individual children, families, and communities submit requests, service coordinators assisted with inquiries and helped prepare requests related for necessary products, services, or supports. These coordinators were funded by ISC and are staffed by First Nations members, tribal councils, regional health authorities, and First Nations non-governmental organizations.

Regions were responsible for intake, adjudication and payment processing in addition to coordination with service providers. For group requests, regions established and managed funding agreements with recipients. Regions do not have the authority to deny requests; any requests that couldn't be approved were escalated to Headquarters (HQ) for adjudication. Escalated requests were either approved or denied based on delegated decision-making authority from the First Nations and Inuit Health Branch (FNIHB) Assistant Deputy Minister (ADM).

Requests are processed using the Jordan's Principle Case Management System (JPCMS), which is considered the system of record for adjudication decisions. Approved individual request payments are processed in SAP (the system of record for payments and associated financial authorities). Approved group request payments are processed through the Grants and Contributions Information Management System (GCIMS) (the system of record for payments and associated financial authorities). These systems operate independently and are not interconnected.

1.4 Overview of Jordan's Principle funding

Funding for Jordan's Principle is held in a special purpose allotment (SPA) to ensure expenditure control. The funding is exclusively to be used to support Canada's implementation of Jordan's Principle, pursuant to CHRT orders and Treasury Board decisions. The SPA ensures that funding allocated to Jordan's Principle is not used to support other programs or initiatives. The related funding flows through contribution agreements to fund group requests, service coordinators and some individual requests, or through Vote 1 O&M funding for individual requests delivered through direct reimbursement payments to families, individuals and service providers. While Jordan's Principle does not have its own terms and conditions (other than for capital-related 2021 CHRT 41 requests), funding for approved requests closely aligns with existing departmental terms and conditions, including, for instance, the Primary Health Care Authority.

Jordan's Principle expenditures for the years between April 2020 and March 2024 totaled $3.7 billion, with an additional budgeted baseline funding of $788.33M/year for FY2024-25 to FY2027-28, which includes internal services and centrally held items. Of the FY2023-24 expenditures, approximately 88% was funded through Vote 10 – Grants and Contributions. Vote 10 funding is primarily used to fund approved group requests and is delivered through existing contribution agreements with the organizations submitting the requests who may use the funding to support delivery of various services. However, some individual requests are also funded through Vote 10 in circumstances where a service coordination organization (i.e. First Nation, Tribal Council, Health Authority, etc.) acts as an intermediary between the family submitting the request and ISC. The remaining 12% was funded through Vote 1 – Operating Expenditures, which is primarily used for individual requests for products, services and supports, and funding is delivered through direct reimbursement to families or vendors (i.e. service providers). Table 2 provides a summary of the individual and group expenditures from April 1, 2020, to March 31, 2024.

| Expenditures in Millions ($) | 2020-21 | 2021-22 | 2022-23 | 2023-24 | Total |

|---|---|---|---|---|---|

| Vote 1 – O&M | $48.57 | $74.77 | $120.03 | $224.51 | $467.88 |

| Vote 10 – G&C | $490.74 | $532.28 | $825.03 | $1,428.76 | $3,276.81 |

| Total | $539.31 | $607.05 | $945.06 | $1,653.27 | $3,744.69 |

| Note: These figures represent the Jordan's Principle expenditures as of March 31, 2024, and do not include program administration O&M costs. | |||||

1.5 Overview of trends in the implementation of Jordan's Principle

Year-over-year growth in request demand

From fiscal year (FY) 2020-21 to fiscal year 2023-24, Jordans' Principle has experienced growth in the number of individual requests and group requests submitted. Figures 1 and 2 present an overall view of the total number of individual and group requests submitted over the period. As seen, the number of submitted requests grew at an annual average growth rate of approximately 57% per year.

Figure 1: Individual requests from FY 2020-21 to FY 2023-24

Notes: 1) Excludes requests for Inuit Children and service coordination; 2) Requests submitted were assigned to a FY based on initial submission date; 3) Data extracted from the Jordan's Principle Case Management System (CMS) and may not align with other analyses.

Text alternative for Figure 1: Individual requests from FY 2020-21 to FY 2023-24

Figure 1 provides an overview of the number of individual requests submitted from fiscal year 2020–21 to 2023–24;

- In 2020–21, there were 38,273 individual requests.

- In 2021–22, there were 52,374 individual requests.

- In 2022–23, there were 102,124 individual requests.

- In 2023–24, there were 141,266 individual requests.

Based on data from the Jordan's Principle Case Management System (CMS), these figures exclude requests for Inuit children and service coordination, and assign requests to a fiscal year by initial submission date. Data may not align with other analyses.

Figure 2: Group requests from FY 2020-21 to FY 2023-24

Notes: 1) Excludes requests for Inuit Children and service coordination; 2) Requests submitted were assigned to a FY based on initial submission date; 3) Data extracted from the Jordan's Principle Case Management System (CMS) may not align with other analyses

Text alternative for Figure 2: Group requests from FY 2020-21 to FY 2023-24

Figure 2 provides an overview of the number of group requests submitted from fiscal year 2020–21 to 2023–24;

- In 2020–21, there were 2,538 group requests.

- In 2021–22, there were 3,199 group requests.

- In 2022–23, there were 6,693 group requests.

- In 2023–24, there were 10,877 group requests.

Based on data from the Jordan's Principle Case Management System (CMS), these figures exclude requests for Inuit children and service coordination, and assign requests to a fiscal year by initial submission date. Data may not align with other analyses.

As both individual and group requests may include various products, services, these have also increased. Figures 3 and 4 below demonstrate the growth in demand for products, services and supports for both individual and group requests.

Figure 3: Total products, services, and supports for individual requests from FY 2020-21 to FY 2023-24

Notes: 1) Excludes requests for Inuit Children and service coordination; 2) Requests submitted were assigned to a FY based on initial submission date; 3) Data extracted from the Jordan's Principle Case Management System (CMS) may not align with other analyses

Text alternative for Figure 3: Total products, services, and supports for individual requests from FY 2020-21 to FY 2023-24

Figure 3 provides an overview of the number of approved products, services, and supports for individual requests from fiscal year 2020–21 to 2023–24;

- In 2020–21, there were 37,035 approved products, services, and supports for individual requests.

- In 2021–22, there were 57,819 approved products, services, and supports for individual requests.

- In 2022–23, there were 129,167 approved products, services, and supports for individual requests.

- In 2023–24, there were 201,530 approved products, services, and supports for individual requests.

Based on data from the Jordan's Principle Case Management System (CMS), these figures exclude requests for Inuit children and service coordination, and assign requests to a fiscal year by initial submission date. Data may not align with other analyses.

Figure 4: Total products, services, and supports for group requests from FY 2020-21 to FY 2023-24

Notes: 1) Excludes requests for Inuit Children and service coordination; 2) Requests submitted were assigned to a FY based on initial submission date; 3) Data extracted from the Jordan's Principle Case Management System (CMS) may not align with other analyses.

Text alternative for Figure 4: Total products, services, and supports for group requests from FY 2020-21 to FY 2023-24

Figure 4 provides an overview of the number of approved products, services, and supports delivered for group requests from fiscal year 2020–21 to 2023–24;

- In 2020–21, there were 302,619 approved products, services, and supports delivered for group requests.

- In 2021–22, there were 455,426 approved products, services, and supports delivered for group requests.

- In 2022–23, there were 1,144,973 approved products, services, and supports delivered for group requests.

- In 2023–24, there were 1,968,517 approved products, services, and supports delivered for group requests.

Based on data from the Jordan's Principle Case Management System (CMS), these figures exclude requests for Inuit children and service coordination, and assign requests to a fiscal year by initial submission date. Data may not align with other analyses.

Increase in breadth of scope of products, services and, supports

The underlying issue that led to the creation of Jordan's Principle is the persistent gap in access to an adequately funded continuum of services for First Nations children. Ongoing gaps in the provision of services by provinces and territories combined with the continued absence of community-based services has led First Nations families to increasingly seek assistance through Jordan's Principle. The steep incline in requests and associated expenditures since 2021 is also attributable to, for instance, the expanded scope and eligibility for Jordan's Principle under CHRT orders and increased awareness of the initiative. The continued rise in request demand may also be explained by the widening of the types of services, products, and supports that are being funded through Jordan's Principle, where request eligibility continues to evolve based on changes to CHRT orders. As an example, in FY2020-21 the number of total products, services, and supports requested was 339,654. In FY2023-24, this number grew to approximately 2.1 million approved products, services, and supports. In FY2023-24, the top five categories by number of requested products, services and supports listed from largest to smallest included: Health Services, Social, Mental Wellness, Education and Economic Supports. It was noted that some components of these expense categories may be covered by other ISC programs including Income Assistance, Assisted Living, Home and Community Care, Non-Insured Health Benefits (NIHB), Elementary and Secondary Education, Education Facilities, and Child Family Services (CFS), among others. Furthermore, since ISC programs are predominately focused for on-reserve products and services, it was noted that demand for Jordan's Principle has increased to address gaps for off-reserve families and children.

Year-over-year growth in costs

The growth in requests has led to continued funding needs to pay for the increasing number of approved requests. As can be seen in Table 3 below, between FY2020-21 and FY2023-24, actual expenditures for Jordan's Principle grew by 207%, from $0.55B to $1.69B, including the departmental salary and administrative costs, which represents approximately 2% of the total expenditures. Considering the 47% average year over year growth rate, FY2027-28 projected expenditures could exceed $7.9B at this trajectoryFootnote 1. However, the introduction of new operational parameters and processes, including the identification of ineligible categories of requests (e.g., certain school-related requests, non-medical supports such as childcare and clothing), should help to shift the current trajectory towards a more sustainable one.

| Expenditures in Millions ($) | 2020-21 | 2021-22 | 2022-23 | 2023-24 |

|---|---|---|---|---|

| Salary and Administration | $13.66 | $17.01 | $27.34 | $41.72 |

| Vote 1 – O&M | $49.01 | $74.60 | $121.72 | $226.78 |

| Vote 10 – G&C | $490.74 | $532.28 | $825.03 | $1,428.76 |

| Total | $553.41 | $623.89 | $974.09 | $1,699.44 |

| Note: These figures represent the Jordan's Principle expenditures as of March 31, 2024, and include program administration O&M costs. | ||||

Figure 5 illustrates the breakdown of expenditures for requests by expense type. As of FY2023-24, expenditures for Health requests accounted for approximately 42% of the total expenditures made for requests.

Figure 5: Expenditures ($ million) by Expense Type

Notes: 1) Limited to original determinations. Appeals and re-reviews of past decisions were excluded; 2) Requests were assigned to a FY based on the decision date at the Regional/HQ level; 3) Excludes Inuit requests and service coordination requests; 4) Approved funding limited to records with approved amounts of ≥$1. The financial information included in this analysis is based solely on approved amounts captured in the Jordan's Principle CMS, and may not reflect actual expenditures and/or match coding from SAP; 5) Requests were collected through the Jordan's Principle Case Management System may not align with other analyses.

Text alternative for Figure 5: Expenditures ($ million) by Expense Type

Figure 5 provides an overview of expenditures (in millions of dollars) by expense type—Health, Social, Education, and Other—from fiscal year 2020–21 to 2023–24;

- In 2020–21, expenditures were: Health ($302.5M), Social ($105.9M), Education ($104.7M), and Other ($9.2M).

- In 2021–22, expenditures were: Health ($243.1M), Social ($140.3M), Education ($126.9M), and Other ($15.0M).

- In 2022–23, expenditures were: Health ($448.0M), Social ($245.3M), Education ($327.9M), and Other ($34.8M).

- In 2023–24, expenditures were: Health ($655.3M), Social ($447.8M), Education ($385.0M), and Other ($56.8M).

These figures are limited to original determinations, as appeals and re-reviews of past decisions were excluded. Requests were assigned to a fiscal year based on the decision date at the Regional or Headquarters level. The data exclude requests from Inuit individuals and those related to service coordination. Approved funding is limited to records with approved amounts of $1 or more. The financial information reflects only approved amounts captured in the Jordan's Principle Case Management System (CMS) and may not represent actual expenditures or align with SAP coding. Additionally, data collected through the CMS may not align with other analyses.

Continued need for off-cycle funding requests to meet demand

Jordan's Principle is a demand-driven initiative subject to oversight by the CHRT. This has contributed to ISC's limited ability to implement policy and operational parameters and accurately estimate the required funding for a given FY. Figure 6 below shows a breakdown of the overall funding between FY2020-21 and FY2023-24, broken down by funding allocation available at beginning of each year and actual expenditures at end of year.

Figure 6: Initial Budget Allocation vs Actual Expenditures ($ million)

Notes: 1) Limited to original determinations. Appeals and re-reviews of past decisions were excluded; 2) Requests were assigned to a FY based on the decision date at the Regional/HQ level; 3) Excludes Inuit requests and service coordination requests; 4) Approved funding limited to records with approved amounts of ≥$1. The financial information included in this analysis is based solely on approved amounts captured in the Jordan's Principle CMS, and may not reflect actual expenditures and/or match coding from SAP; 5) Requests were collected through the Jordan's Principle Case Management System may not align with other analyses.

Text alternative for Figure 6: Initial Budget Allocation vs Actual Expenditures ($ million)

Figure 6 provides a comparison between initial budget allocations (Forecast Need) and actual expenditures (in millions of dollars) from fiscal year 2020–21 to 2023–24;

- In 2020–21, the forecast need was $404.1M, while actual expenditures reached $522.2M.

- In 2021–22, the forecast need was $404.1M, while actual expenditures reached $524.6M.

- In 2022–23, the forecast need was $772.8M, while actual expenditures reached $1,081.3M.

- In 2023–24, the forecast was $793.9M, while actual expenditures reached $1,615.1M.

These figures are limited to original determinations, as appeals and re-reviews of past decisions were excluded. Requests were assigned to a fiscal year based on the decision date at the Regional or Headquarters level. The data exclude requests from Inuit individuals and those related to service coordination. Approved funding is limited to records with approved amounts of $1 or more. The financial information reflects only approved amounts captured in the Jordan's Principle Case Management System (CMS) and may not represent actual expenditures or align with SAP coding. Additionally, data collected through the CMS may not align with other analyses.

2. About the audit

The Audit of Jordan's Principle was included in Indigenous Services Canada's Risk-Based Audit Plan for 2022-23 to 2023-24, which was presented to the Departmental Audit Committee and approved by the Deputy Minister in May 2023.

2.1 Why it is important

The audit was identified as a priority because the Department identified several risks for Jordan's Principle related to the following:

- There is a risk that the Management Control Framework has not been revisited or updated to support the current implementation of Jordan's Principle.

- There is a risk that key operational and financial controls for processing Jordan's Principle requests are not designed, implemented and/or operating effectively, impacting compliance with the Canadian Human Rights Tribunal (CHRT) orders, the Financial Administration Act (FAA), and applicable Treasury Board Policies and Directives.

- There is a risk that the products, services and supports funded through Jordan's Principle may also be funded and/or provided by other Indigenous Services Canada (ISC) programs, other Federal Departments, and/or Provinces and Territories.

- Due to the evolving nature of the implementation of the Initiative, there is a risk that some payments made under Jordan's Principle do not appropriately fit within the terms and conditions of existing ISC programs.

2.2 Audit objective

The objective of the audit was to provide assurance on the adequacy of:

- The Management Control Framework (MCF) to support the current implementation of Jordan's Principle; and

- Processes in place to minimize overlap of Jordan's Principle funding.

2.3 Audit scope

The audit examined the activities undertaken by ISC to implement Jordan's Principle through the period of January 1, 2022 (implementation of Back to Basics (B2B)), to March 31, 2024, and included an assessment of:

- Mechanisms to govern and oversee the implementation of Jordan's Principle and management of Jordan's Principle funding;

- Elements of the management control framework (MCF), including delegation and assignment of roles and responsibilities, policies and procedures and the supporting guidance, tools, and training materials in place to enable the implementation of Jordan's Principle.

- Roles and responsibilities of legal services in relation to the implementation of Jordan's Principle;

- Key financial controls to ensure compliance with the FAA, financial and spending authorities, and applicable Treasury Board Directives and Policies, including the Policy and Directive on Transfer Payments, Policy on Financial Management, and Directive on Delegation of Spending and Financial Authorities;

- Key operational controls to support the effective and timely processing of individual and group requests throughout their lifecycle while ensuring errors are mitigated, as well as compliance with the CHRT orders; and

- Mechanisms for timely identification and to minimize funding overlap between Jordan's Principle and existing services and programs delivered by other ISC programs, other Federal Departments, and/or Provinces and Territories.

The audit fieldwork was performed from April 2024 to November 2024. The audit scope included activities performed in FNIHB-HQ and regional offices. There are eight ISC regional offices involved in the implementation of Jordan's Principle across the country (Alberta, Atlantic, British Columbia, Manitoba, Northern, Ontario, Quebec and Saskatchewan). During the planning phase, different regional approaches and processes were observed in each region. Given this, all eight regions were audited to understand the particularities of their processes and tools. This included testing a sample of Jordan's Principle files from each of the regions. Furthermore, regional site visits were conducted with First Nations Organizations to provide supporting insights related to risk, governance, and control.

The audit excluded departmental activities related to the implementation of the policy-based Inuit Child First Initiative which modeled on Jordan's Principle, but targets Inuit children. The Inuit Child First Initiative is not compelled by the CHRT. orders. Assessment of the negotiations of long-term reform and all litigation (i.e. the non-compliance motion, etc.) are also outside the scope of the audit. A sample of selected First Nations communities and organizations were consulted to gather key insights and perspectives as key stakeholder groups within Jordan's Principle. However, activities performed by First Nation communities and organizations were not in scope.

2.4 Audit approach and methodology

The audit was conducted in accordance with the requirements of the Treasury Board Policy on Internal Audit and followed the Institute of Internal Auditors International Professional Practices Framework. The audit examined sufficient, relevant evidence and obtained sufficient information to provide a reasonable level of assurance in support of the audit conclusion. The main audit techniques used included:

- Interviews – Performed approximately 60 interviews across Headquarters (HQ) and regional staff management teams.

- Process review – Performed approximately 27 process walkthroughs across HQ and regional staff management teams related to processing individual and group requests as well as financial payments.

- File testing – Performed operational and financial control file testing procedures across a sample of 320 requests (160 group requests and160 individual requests).

- Documentation review – Inspected approximately 8,550 operational documents and file testing artifacts provided by HQ and regional staff management teams.

- Data analytics – Performed data analytics activities examining approval, denial rates and expenditures across various expense categories.

The approach used to address the audit objective included the development of audit criteria, against which observations and conclusions were drawn. The audit criteria can be found in Annex B.

2.5 Other Jordan's Principle reviews and Integrated Action Plan

In addition to the Audit of Jordan's Principle, several internal and external reviews were conducted, resulting in recommendations affecting key elements of the initiative's implementation. In early 2023, prior to these reviews, CFRDO completed internal control testing and improvement work.

In response to the recent audit and reviews, First Nations and Inuit Health Branch (FNIHB) management developed an Integrated Action Plan to consolidate all recommendations and action items into a single, coordinated dashboard. This approach supports timely follow-up, reduces duplication, and identifies opportunities for collaboration.

The Integrated Action Plan draws from the following sources:

- CFRDO Internal Control File Review – 14 recommendations (2023-24)

- Independent Financial Management Review – 20 recommendations (2024)

- Ombud's Annual Report – 6 recommendations (2023-24)

- Internal Audit of Jordan's Principle – 4 recommendations (2023-2025)

In total, 44 recommendations were analyzed, with common themes identified across them, including processes and procedures, financial management, technology, people management, and communication strategy. As of January 23, 2025, management reported that 55% of the Integrated Action Plan recommendations and action items have been completed.

3. Key findings and recommendations

The audit found that, given the increase in requests and associated costs combined with limited departmental human and financial resources, the implementation of Jordan's Principle, in accordance with the Back to Basics (B2B) approach observed during the audit period, clearly demonstrates that the current state of unclear eligibility of expenditures and evolving scope of approved products and services is unsustainable.

While several factors contributing to this growth were identified, the audit also highlighted numerous opportunities to enhance the Management Control Framework (MCF). These enhancements could help mitigate sustainability challenges, reduce the risk of errors and reduce the volume and scale of unwarranted requests resulting from the reduction of administrative barriers to accessing support.

The audit's key findings and recommendations are further detailed throughout the following sections:

- 3.1 Adequacy of the management control framework;

- 3.2 Adequacy of internal controls in place to support the implementation of Jordan's Principle;

- 3.3 Technology needs and current process inefficiencies;

- 3.4 Identification and rectification of potential funding overlap; and

- 3.5 Measuring and reporting on progress.

3.1 Adequacy of the management control framework (MCF)

Background

A well-designed MCF can ensure that all staff adhere to the same standards, policies, and procedures, promoting consistency in service delivery. It also facilitates effective coordination and communication among stakeholders. Clearly defining roles, responsibilities, and authorities for stakeholders supports accountability and oversight. It aids in monitoring performance, maintaining compliance, and holding leadership teams and relevant parties accountable for their actions. A well-structured MCF supports risk mitigation, proactive issue resolution, and transparency in decision-making and resource management, raising the confidence of stakeholders such as the public, partners, and other governmental entities.

Risk

There is a risk that the MCF has not been revisited or updated to support the implementation of Jordan's Principle. This could result in inconsistencies in its national application, creating challenges in establishing shared expectations and standards among stakeholders. It may also hinder the ability to measure effectiveness and identify overlaps with other programs and services and/or other levels of Government, ultimately affecting the Department's ability to achieve the intended outcomes of Jordan's Principle including:

- First Nations children have improved access to products, services and supports;

- First Nations children have access to products, services and supports in a timely manner;

- First Nations children's health, social and/or education needs are met; and

- Indigenous Peoples are physically well.

Finding

In FY2018-19, the Department developed a MCF for Jordan's Principle, which was developed by FNIHB HQ to help guide the national implementation of Jordan's Principle. The purpose of the MCF was to design and refine control processes, structures and tools that reflect a standard of control that is both "adequate" and "effective" to mitigate potential risks and that can be readily audited. The MCF included multiple components, such as revised delegation of authority instruments for approval decisions regarding request processing and payments, establishment of operational guidance and standard operating procedures to support efficient, effective, and consistent processing of requests, development and delivering of training programs, and redefining the Jordan's Principle governance structure with clear identification of leadership and the associated roles and responsibilities.

Following the 2019 Indigenous Services Canada (ISC) internal audit of Jordan's Principle, management committed to addressing the identified recommendations and risks by updating the MCF; however, since that time, it has not since been revisited. Rather, the audit observed that several elements of the MCF were removed as part of the B2B approach, including Standard Operating Procedures (SOPs). The SOPs were replaced by the B2B approach document and operational bulletins that were released on an ad hoc basis to provide guidance on how to treat issues that emerged.

Regions interviewed informed auditors that the guidance was insufficient and there was lack of clarity on who should adjudicate what requests. The audit also observed that there was training in place that was designed to augment the B2B documentation; however, the audit observed through interviews that certain regions felt it was overly simplistic and did not address the need for guidance on complex scenarios in the B2B approach or other policy instruments.

Several regions understood that the responsibility to develop and issue guidance for implementing B2B was with Headquarters (HQ); however, to address gaps, many regions put together their own guidance packages. Furthermore, auditors noted that roles and responsibilities regarding the development of guidance were not documented.

The Jordan's Principle Operations Committee (JPOC), which includes representatives from the parties to the CHRT complaints, has contributed to the development of operational guidance and supported implementation by monitoring progress and informing stakeholders. The committee reports to the Consultation Committee on Child Welfare (CCCW) and includes both First Nations and ISC regional representatives. While JPOC has been the national venue for external coordination, internally, Jordan's Principle was addressed through broader First Nations and Inuit Health Branch (FNIHB) governance structures, such as the Senior Management Committee. These discussions have focused on issues such as managing the backlog, implementing corrective actions, supporting long-term policy and program changes, clarifying provincial and territorial roles, and assessing cross-program impacts.

Overall, without an effective MCF, the Department had limited mechanisms to ensure nationally consistent implementation of Jordan's Principle, other than regional meetings chaired by Headquarters. This created challenges in ensuring all staff were working with the same expectations and standards and limited the ability to measure effectiveness of the initiative and identify potentially duplicative funding as a result of overlap with other programs and services and/or other levels of Government.

Recommendation #1

The Assistant Deputy Minister (ADM) of Jordan's Principle should establish a risk-based management control framework with clearly defined roles, responsibilities, and guidance for those involved in delivering and overseeing the implementation of Jordan's Principle across the Department.

Audit considerations:

The Department should revisit the B2B approach to ensure that there are appropriate measures in place to implement Jordan's Principle in a manner consistent with CHRT orders while complying with the Financial Administration Act (FAA) and applicable TB Policiesrelevant to the stewardship and safeguarding of financial resources.

Additional considerations related to management control framework and specific control gaps are outlined in section 3.2 below.

3.2 Adequacy of internal controls in place to support the implementation of Jordan's Principle

Background

Internal controls include the policies and operating procedures (both manual and automated) designed to provide reasonable assurance that an organization's objectives are achieved and that risks are contained within acceptable levels. Internal controls may include activities designed to mitigate risks related to the effectiveness and efficiency of operations; reliability of reporting; and compliance with laws, regulations, and internal policies and procedures.

In January 2022, the Department replaced its existing SOPs with the B2B policy. The intent was to ensure that the implementation was non-discriminatory; centered on the needs and best interests of the child; took into consideration the distinct circumstances of the child's community; was simple to access, timely, and minimized the administrative burden on applicants.

The audit anticipated the presence of sufficient internal controls to support the implementation of Jordan's Principle under the B2B policy. These controls were expected to adequately mitigate risks associated with processing and funding both individual and group requests.

Risk

There is a risk that key operational and financial controls for processing requests were not designed, implemented and/or operating effectively, impacting adherence with the CHRT orders, the FAA, and applicable Treasury Board Policies and Directives.

Finding

Overall, the audit observed that internal controls in place between January 1, 2022 and March 31, 2024, were inadequate.

The audit observed that some internal controls were designed and generally followed consistently. For example, regions escalating requests that were outside their approval authority for assessment by the national review committee. Furthermore, training materials were rolled out from HQ with best practices for utilizing the Jordan's Principle Case Management System (JPCMS) as the key tool for managing requests worked well. However, a number of areas for improvement were identified across the following areas:

- Lack of risk management framework;

- Intake and backlog management processes;

- Review and determination of requests;

- CHRT timeline compliance measurement and reporting;

- Payment processing;

- Recipient monitoring; and

- File quality review and continuous improvement.

Lack of a risk management framework to support the implementation of Jordan's Principle

In implementing B2B policy with the intent to not delay decision making based on administrative barriers, a number of existing SOPs were removed, including critical operational documents such as:

- guidance for processing requests, which included the intake and determination of individual and group requests; and

- guidance respecting required supporting documentation for both individual and group requests, including quotes and cost estimates to assess the reasonableness of the cost.

Under the B2B policy, quotes and cost estimates were not required. The documentation requirements were significantly decreasedFootnote 2. Under this policy, the only requirement was a letter of support from a registered professional, community elder or non-registered professional where applicable, child eligibility documentation, and documented consent. In some cases, supporting documentation was accepted by non-registered professionals like family support workers. Under the policy, the requestor determined the vendor of choice (regardless of cost) and self-assessed the urgency level, which impacted the Department's required response time. While cost was not required for determination purposes, it was required for payment and group request funding approvals per FAA requirements.

Another example of notable changes under the B2B approach was clinical case conferencing. This was a process whereby the Department coordinated healthcare professionals and other stakeholders to collaboratively develop comprehensive care plans for children with complex needs. Under the B2B approach, this process was only applied when reasonably necessary. As such, intradepartmental collaboration to assess whether a request could be better suited to other programs and services was discontinued. Clinical case conferencing can also occur in instances where Jordan's Principle officials can consult with the prescribing or referring practitioner if there are follow-up questions or clarifications needed for a given recommended product or service.

Despite the changes in policy and removal of prior SOPs, the audit observed that the Department had not put in place a risk management framework to ensure risks were identified, evaluated, addressed, and appropriately monitored. Rather, the Department and the Parties agreed to implement B2B without conducting a risk and impact assessment to understand the risks and exposures to the Department associated with this decision.

Furthermore, under the B2B policy, there was a high degree of reliance on individual employees making appropriate decisions along the request lifecycle, such as prioritizing requests during intake or deciding on what to approve or escalate. However, without a risk management framework that guides the Department's tolerance of what was acceptable or not acceptable, the Department relied on each individual's interpretation of acceptable risk. This increased the probability of inconsistent decisions being made on what was approved or denied. Examples of inconsistencies are further outlined in the review and determination section.

The audit also observed that a formal assessment of risks to evaluate the potential consequences of the B2B policy and the removal of SOPs was not performed. Several procedures were removed, which included controls that were preventive in natureFootnote 3. Preventive control activities increase the administrative burden of processing a request, which in turn can increase processing timelines. As such, the Department was constrained in its ability to mitigate risks using preventive controls while respecting the CHRT orders. However, the audit did not observe compensating controls to reduce risks related to the removal of key processing steps. Compensating controls could include detective and corrective controls that are designed to identify and remediate negative events after they have occurred. They may not be as effective as preventative controls; however, they can still be effective at reducing the overall risk exposure. Performing a formal risk assessment would provide insight into the Department's residual risks and help identify appropriate compensating controls to reduce risks to an acceptable level.

Observed control gaps are described in the following subsections below in more detail.

Intake and backlog management processes

Requests can be submitted by families, caregivers, or service coordinators through various channels, including emails, phone calls, or fax. Once a request is received by the Department, it is entered into JPCMS, the system of record for determination. At the time, requestors self-assessed the level of urgency, and a preliminary assessment of the request and child eligibility was performed by the intake officer. If the required documentation was insufficient (per B2B policy requirements), the intake officer followed up to obtain the missing documentation. Once it was determined that all required information was received, the request was entered a queue for determination. The backlog consists of all requests that have been entered into JPCMS by the intake officer, regardless of whether they are ready for determination.

Key audit insights:

First Nations have expressed concerns that some urgent requestors may have incorrectly labelled their requests as urgent, contributing to the backlog of requests and untimely processing of truly urgent requests. Overall, communities have expressed frustration with lack of clarity over what is considered urgent. Many requests identified as urgent by requestors were for necessities of life such as rent, groceries or urgent medical care. However, below there are many examples of the types of other requests that were classified as urgent by the requester unnecessarily, including:

Below are examples of the types of requests that were classified as urgent:

- Furniture

- Gaming consoles

- Gym memberships

- Laptops, desktop computers, software

- Lawn mowers

- Medical transportation

- Medical instruments

- Modelling headshots

- Office supplies and cell phones

- Palliative care

- Pet expenses

- Respite care

- Snow mobiles

- Sporting equipment

- Summer camp registration

Furthermore, visited First Nations expressed concerns that some urgent requests may be wrongly labelled as urgent, which are contributing to the backlog of requests, resulting in untimely processing of critical requests. Overall, communities have expressed frustration with lack of clarity over what is considered urgent.

The audit observed that there was a control gap related to the triage of urgent requests. Under the B2B policy, requests were to be treated as classified by the requestor (urgent vs. non-urgent). For instance, if the requestor classified a request as urgent, the Department needed to treat it accordingly. Per CHRT requirements, urgent requests needed to be processed within 12 hours for individual requests and 48 hours for group requests. The audit observed that there was a varying degree of urgency amongst requests. For example, requests that requestors labelled as urgent ranged from what would appear to be less time sensitive items such hockey equipment, sports camp registration, to what would appear as more critical items such as palliative care, medical transport, etc.

Under the B2B policy, the definition of urgent was eliminated in favour of self-declaration of urgency by the requestors. Furthermore, there was no guidance for staff to support determining priority/time sensitivity. Therefore, intake officers had to use personal judgement to prioritize request processing.

In response to the First Nations Child & Family Caring Society's (Caring Society) non-compliance motion filed on December 12, 2023, the Government of Canada submitted a cross-motion to the Canadian Human Rights Tribunal (CHRT) on March 15, 2024. The cross-motion sought several measures, including: the co-Development of Objective Criteria: Canada proposed that the parties collaborate to establish objective criteria for identifying urgent requests under Jordan's Principle

In addition to challenges in prioritizing urgent requests, the audit identified a control gap in the mechanism used to measure pending requests— referred to as 'backlog' by management. Specifically, there was no clear process to quantify the expected volume of requests received via email, fax and phone that had yet to be entered into JPCMS, the system of record for adjudication. While some regions did the data entry at intake, others only entered data into JPCMS once the file was complete and ready for determination. There was no standard process or guidance for measuring and reporting on the backlog. At the time, the total request backlog figures consisted only of requests in JPCMS, which excluded requests for which intake was incomplete. There was not a readily available report to count the number of requests pending intake. To address this issue, some regions manually counted requests pending data entry into JPCMS and reported to HQ to consolidate the view of the total backlog pending decision. HQ management confirmed they did not have an accurate, complete and up to date view of backlogged requests pending intake. Without an accurate calculation of the total backlog pending determination, management lacked the ability to accurately, completely, and in a timely manner, examine the true workload.

As mentioned above, the intake process relied heavily on manual tracking of requests received via email, fax and phone. Four of the eight regions expressed concern that the same child's need could be submitted via multiple individual requests from different care givers, with limited controls to identify and address this duplication. Similarly, an individual request could be submitted for goods and services also captured by an existing group request. As such, the audit observed that there were insufficient compensating controls related to preventing, detecting and correcting of potential duplicate requests.

Considering the CHRT compliance timelines, it was not feasible for intake officials to perform adequate due diligence regarding potentially duplicative requests. However, there are no CHRT requirements that prohibit follow-up and monitoring mechanisms in place to detect and correct potential instances of duplicate funding. The audit observed that JPCMS had limited application controls and reporting capabilities to inform this type of follow-up analysis, risking potentially duplicative payments to requestors at both individual and community levels. Instead, duplicate requests were manually identified on a best-effort basis using informal checks and Microsoft Excel sheets to help prevent approving requests that were duplicative.

Review and determination of requests

Once intake was complete, the ISC regional focal point informed the requester that a determination was underway. Using all the information gathered in the intake process and upon evaluation of the request, the focal point took one of the following steps:

- Determined if the request was admissible within its authority (refer to section 1.3 for details);

- Consulted with the National Review Team; or

- Escalated the request to the National Review team.

Either within region or within the National Review Team, the determination of a request relied on a 'common sense' approach, per the B2B policy. A lack of written parameters and reliance on official's judgment carried a risk of inconsistent decision making, which was noted in each of the regions. Examples of inconsistent decision making and some of the constraints are further expanded upon in the paragraphs below.

The audit observed several control gaps for which there were insufficient compensating controls in place related to determining requests. Furthermore, during the decision of whether a request should be approved within the region or escalated to the national review committee, the audit observed a control gap related to consistent decision making with respect to which requests were to be approved within the region or escalated.

Similarly, a control gap was observed related to consistent decision-making of escalated requests. Since there were no defined expenditure admissibility criteria, determination decisions used a 'common sense' approach, both within regions and within the national review committee. The audit observed inconsistent decision-making using this approach. Approving a similar request in one region but not another (or in one community but not another) risked perceptions of inequity and inconsistency, potentially undermining trust in the process and augmenting the risk of reputational harm to the Department.

Below are examples of products, services, and supports that were approved in some cases and denied in other cases, with insufficient explanation on file to account for the discrepancy. Furthermore, visited First Nations expressed concerns with the lack of clarity around admissible expenditures and the lack of defined parameters. As such, requesters were unclear what would get approved or denied.Key audit insights:

For approved requests, the audit observed a control gap related to sufficiency and adequacy of documentation saved within the system of record to justify the approval and for future reference. In alignment with the B2B policy, approved requests should have included a professional letter of support (or an equivalent recommendation from a community-authorized elder); documented consent; an assessment of child eligibility, and documentation associated with the approval decision. The audit observed instances where approved requests did not include the required information saved within JPCMS. Moreover, there were varying practices across regions for labelling, storing, and saving key documentation in JPCMS, which resulted in difficulties in obtaining a holistic view of the decision-making authorities for any given decision. In other words, the Department does not have a clear view of tracing approved requests and supporting authorities to the expenditures administered, and vice versa.

Despite JPCMS information management best practices being in place via training from HQ, these best practices were often not followed. Given the nature of Jordan's Principle, there may be a future need to refer to the files to understand the approval rationale and how requests were supported. Insufficient documentation may hinder the Department's ability to understand and support approval decisions. The 2019 internal audit also outlined similar observations related to incomplete and inconsistent approaches to saving key documentation, where a recommendation was provided to allow for information to be found more easily for future references.

Additionally, there were allowances under B2B policy to process a request without the minimum required documentation (e.g. letter of support from regulated professional). For example, letters of support from unregulated professionals/persons were accepted as a temporary measure. There was an expectation to follow up afterwards to verify that an appropriate professional/person was providing assessment of need and/or delivering the services. However, there were no mechanisms to follow up to receive the missing documentation. Moreover, there was limited resources to address documentation gaps, after the fact even if such a mechanism was in place. Overall, the minimum requirements were in line with the B2B approach which focused on making Jordan's Principle simple to access and minimizing the administrative burden on families. The audit observed a control gap related to follow-up activities to address documentation that was not substantially complete. These follow-up processes were not consistently observed. Inconsistent follow-up on the required supporting documentation risked unqualified individuals providing assessments of a child's need, products, or services, potentially compromising the quality of care. Furthermore, given the requirement to use the service provider of the requestor's choice, there was no formal mechanism to prohibit vendors of concern from rendering services approved for funding.

CHRT timeline compliance measurement and reporting

The CHRT has set the timelines that the Department needs to follow for adjudicating requests. As outlined in Figure 7 below, compliance with CHRT imposed timelines is measured using the point in time at which sufficient information is provided by the requestor to make a decision and the decision date (e.g. when written notice is provided to the requestor). Pursuant to this order, ISC also tracks the time from the submission of a request to its determination, ensuring that decisions are made without undue delay. Regular reports are produced by the Department to measure and report against these timelines, which are reviewed internally by management as well as by the Parties.

Text alternative for Figure 7 – CHRT timeline compliance

Figure 7 provides an overview of the CHRT timeline compliance process for requests made under Jordan's Principle;

- The process begins with the Initial Request, where a request is submitted.

- During the Intake stage, the request is acknowledged by the responsible authority and entered into the JPCMS system.

- In the Review stage, the request is assessed to determine eligibility once deemed complete.

- The Determination stage follows, where eligibility is confirmed, a decision is made, and the requester is notified.

- If approved, the Request Fulfilled stage involves the delivery of products, services, or supports.

- Finally, Payment Processing activities take place for both individual and group requests.

- Two optional stages, Escalation and Appeals may occur where applicable.

The CHRT timeline measurement begins at the Review stage ("Clock starts") and ends at the Determination stage ("Clock stops").

The audit observed several control gaps for which there were insufficient compensating controls in place related to measuring and reporting timeline compliance. There were key date stamps that were used by the Department to measure compliance with the CHRT timelines. Submission date, which is the point in time where all required documentation is provided, and decision date, which is when a decision is made by a Jordan's Principle official, and the requestor is notified. The audit observed that JPCMS does not automatically generate submission and decision dates, rather this is a field that is manually entered by the official based on processing milestones achieved (e.g. submission date entered at point where determined that sufficient information is provided).

The audit found gaps in tracing the date stamps to supporting documentation. Documentation in many cases was an email from ISC to the requestor indicating that the request has been submitted for determination. However, there were instances where the date of the email communicating that the request was submitted was inconsistent with the date stamp in JPCMS. There were also several examples where the audit observed inconsistencies between the decision date in the system and the date of the decision email sent to the requestor. Furthermore, there were no standards for saving/storing key supporting artifacts, such as submission and decision emails. Rather, the documents have to be opened up and examined for relevance to the date stamp, making traceability an onerous, manually intensive process.

Payment processing

When a request was approved, ISC had a variety of mechanisms to process payments. One mechanism included a reimbursement model, which was primarily used to process payments associated with individual requests. Under this approach, after a request was approved, the requestor submitted an invoice and direct deposit information to receive payment for the approved item. Under another approach, ISC had also set up accounts with approved vendors that billed ISC directly for the services provided.

Group request approvals were primarily funded through contribution agreements with First Nations partners and community organizations. ISC delivered funding in accordance with the terms and conditions of the contribution agreement, and the recipient distributed the funding based on the community's proposal outlined in the group request. In many instances, the group request funding was provided to supplement gaps within existing ISC programs and leverages the terms and conditions of existing contribution agreements.

The audit expected that payments made for approved requests would have been completed in accordance with the FAA, as well as applicable Treasury Board policy instruments, including the Directive on Payments, and the Directive on Delegation of Spending and Financial Authorities. Furthermore, in accordance with the Treasury Board Policy on Financial Management, the audit expected that there would have been a risk-based system of internal control in place for payments made under Jordan's Principle with appropriate monitoring activities in place to assess the effectiveness of the internal control processes.

As described in the table below, the audit observed several areas for improvement regarding the internal controls over payments made for approved individual and group requests.

| Control weakness observed | Why the observed weaknesses matter |

|---|---|

Expenditure initiation and commitment authorities (FAA section 32)

|

Incomplete expenditure initiation and commitment authority documentation risks non-compliance with the Treasury Board Directive on Delegation of Spending and Financial Authorities or appropriate departmental authorities. Risk that Jordan's Principle requests will not have sufficient unencumbered balance available before entering into a contract or other arrangement. Without cost information, approving requests without a cost contravenes payment official's delegated authority under section 32 of the FAA. |

Transaction authority

|

Only individuals with appropriate transaction authority should be entering into agreements. Furthermore, the same individual must not exercise both transaction authority and certification authority on the same transaction (per the Treasury Board Directive on Delegation of Spending and Financial Authorities). Appropriately designed segregation of duties controls should have clear expectations of what constitutes transaction authority and how it is to be exercised. |

Certification authority (FAA section 34)

|

Considering instances where payment officials rely on attestations from parents/caregivers, there is an exposure to the Department where payments were made for services, products, supports that were not received by the intended recipient. |

Section 33 quality assurance

|

Providing quality assurance and verifying payments provides a secondary challenge function to ensure that sufficient auditable evidence exists to demonstrate that section 34 has been appropriately carried out, to confirm that payment is not made if it represents an unlawful charge against the appropriation, and to ensure that the payment will not result in an appropriation being exceeded. These steps must be carried out prior to payment for high-risk transactions. Therefore, it is essential that the Department appropriately determine and document the risk of Jordan's Principle individual payments so that appropriate challenge functions are in place and commensurate to the risk. |

Traceability of payments across JPCMS and the payment systems (SAP, Grants and Contributions Information Management System (GCIMS))

|

The lack of traceability impacts the auditability of financial transactions, which is required to demonstrate adherence to key financial authorities prescribed in the FAA and Treasury Board policies. It also leads to inefficiencies due to extra effort required to rekey information cross systems |

|

|

Recipient monitoring

Group requests are considered most appropriate when the needs of children seeking services are more effectively met in the context of the collective needs of a defined group. If the request is approved, a contribution agreement is executed or amended to include the approved funding amount and the corresponding financial and non-financial reports required to report on the use of funds. The contribution agreements are developed to define the various funding initiatives provided by ISC and their terms and conditions.

The Policy on Transfer Payments dictates that administrative requirements for recipients should be proportionate to the risk level. Monitoring, reporting, and auditing should reflect the level of risk, the value of funding in relation to administrative costs, and the risk profile of the recipient.

The recipient report monitoring function for Jordan's Principle involves the use of funds for approved group requests to ensure recipient accountability. Once products, services or supports are purchased, recipients are required to produce annual reports on the actual number of children served and the products and services received through their service delivery via data collection instruments (DCIs). In turn, the Department reviews these reports to verify that the funds were used appropriately (e.g., funding was used for approved products, services, and supports, as well as eligible children, etc.) By maintaining thorough recipient monitoring of the Jordan's Principle DCIs, this function helped to ensure that Jordan's Principle continued to meet the needs of eligible children effectively and sustainably, in addition to supporting Departmental progress tracking and reporting mechanisms.

As such, the audit expected to find a formalized function for monitoring group requests, including officials tasked with monitoring responsibilities, and documented procedures for remediating outstanding reports and taking corrective action to address reporting non-compliance or misuse of funds.

The audit observed several control gaps for which there were insufficient compensating controls in place. For example, the audit noted a control gap related to the establishment of a formal process for monitoring the use of funding administered through group requests. Rather, HQ management mentioned that that there is no practical way for the Department to verify eligibility of the children receiving Jordan's Principle funding, instead it relies on attestations provided by the community. Other than the recipient audits and DCI monitoring, there was no formal monitoring performed in relation to the Jordan's Principle funding administered through community contribution agreements.

The audit noted a control gap related to the observed non-compliance for recipient DCI reporting. More specifically, for FY2020-21 through FY2023-24, DCI compliance was examined. Per GCIMS recipient DCI reporting data, it was observed that non-compliance ranged from 60% to 80% across Canada, impacting the Department's ability to collect and analyze data used to measure progress.

File quality review and continuous improvement

Within the previous SOPs, the quality assurance process served as a key mechanism for the Department to ensure that policies, processes, and standards were being adhered to. It also served as a catalyst for continuous improvement to promote best practices. Under the B2B policy, which no longer included specific quality assurance process as was previously in place under the SOPs, there was a control gap for ensuring key policies, processes and standards were implemented effectively, while promoting continuous improvement initiatives. More specifically, the B2B policy lacked a mechanism to detect and correct potential errors during intake, review, determination, and payment processing activities to ensure accuracy and compliance. Several examined regions confirmed that the quality assurance process was no longer followed under the implementation of the B2B policy.